Foreign demand

What Germany’s Car Crisis Could Mean For The Spanish Property Market

Germany’s car industry is in trouble. That matters for Spain because Germans are not just holidaymakers here — they are one of the most important foreign buyer groups in the Spanish second-home market.

The crisis unfolding in the German car industry is no longer just a boardroom problem in Wolfsburg, Stuttgart, or Munich. It could soon become a property-market problem in Mallorca, Tenerife, and other Spanish destinations that depend heavily on German buyers.

Volkswagen is reportedly weighing deeper job cuts (100,000) and possible German plant closures (4) as part of a dramatic restructuring, whilst the wider industry is struggling with weak demand, high costs, Chinese EV competition, and the painful transition away from combustion engines. Reuters recently reported that VW’s existing job-cutting plans may not be enough, with much bigger reductions under consideration.

The German automotive sector is not just another industry. It is one of the pillars of the German economy, employing hundreds of thousands of people directly and supporting many more through suppliers, logistics, engineering, finance, dealerships, and local services. Germany’s own car-industry lobby, the VDA, warns that the sector faces the potential loss of a further 125,000 jobs by 2035 if Germany and the EU fail to improve competitiveness.

Why this matters for Spain

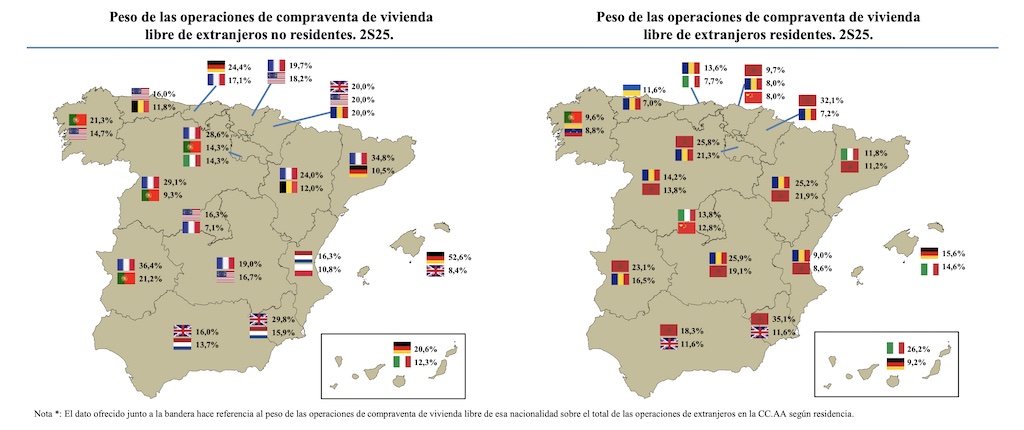

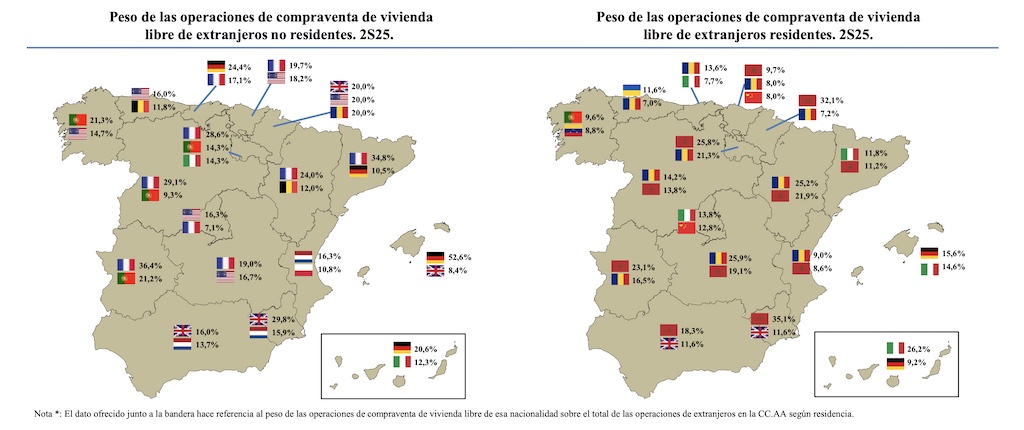

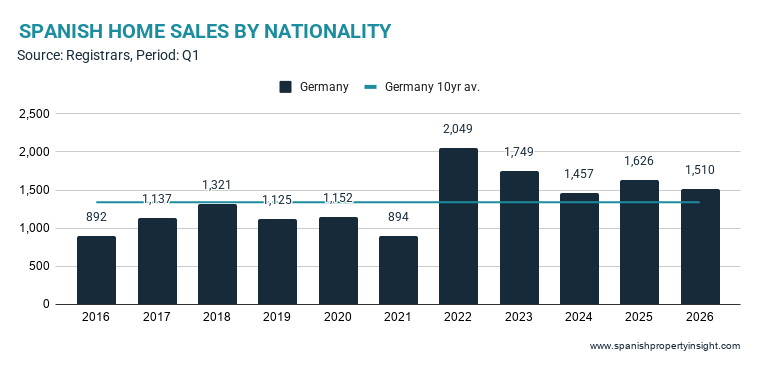

German buyers have long been one of the most important sources of foreign demand for Spanish property. According to notary figures (illustrated in the map above), they dominate the second-home market in the Balearics, where they account for more than half of foreign second-home purchases, and are also the leading group in the Canary Islands. They are number two in Catalonia and Cantabria.

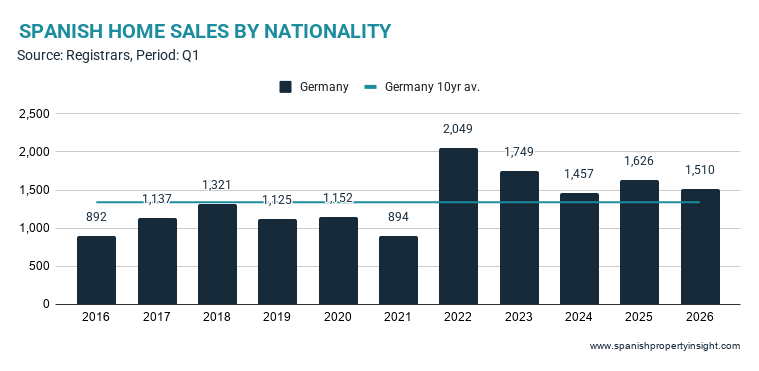

For Spain as a whole, Germans have usually been the second-biggest foreign buyer group behind the British. They briefly took first place in 2021, but since the end of 2025 have slipped into third place behind the Dutch.

Registrar data already show German acquisitions of Spanish property declining year-on-year for three consecutive quarters. That does not yet amount to a slump: German demand remains well above pre-pandemic levels. But the direction of travel is no longer encouraging.

Could early retirement soften the blow?

There is one possible twist. A wave of restructuring in Germany might push some older workers into early retirement, and Spain could look attractive to those with decent pensions, savings, and a desire to make their money go further in the sun.

That may support some demand, especially from wealthier households. But it is unlikely to offset the broader damage if Germany’s industrial crisis deepens. Rising uncertainty tends to make people delay big discretionary purchases, and a second home abroad is about as discretionary as it gets.

The most exposed markets

The Balearics and the Canaries are the most exposed because German buyers play such an outsized role there. Mallorca in particular has spent decades building a market around German demand, from modest apartments to luxury villas. If German confidence and spending power take a serious hit, these markets will feel it first.

Catalonia could also be affected, though German demand there is less dominant and the region has other problems of its own, not least investor-hostile policies and high transaction costs.

The bottom line

A German car-industry crisis will not crash the Spanish property market on its own. Foreign demand is diversified, and British, Dutch, French, Belgian, Nordic, and domestic buyers all matter.

But if Germany’s industrial troubles turn into a wider economic malaise, Spanish second-home markets with heavy German exposure should expect weaker demand, longer selling times, and more price sensitivity. The Germans are not disappearing from Spain. But they may arrive with less confidence, tighter budgets, and a stronger instinct to wait and see.

Germany’s car industry is in trouble. That matters for Spain because Germans are not just holidaymakers here — they are one of the most important foreign buyer groups in the Spanish second-home market.

The crisis unfolding in the German car industry is no longer just a boardroom problem in Wolfsburg, Stuttgart, or Munich. It could soon become a property-market problem in Mallorca, Tenerife, and other Spanish destinations that depend heavily on German buyers.

Volkswagen is reportedly weighing deeper job cuts (100,000) and possible German plant closures (4) as part of a dramatic restructuring, whilst the wider industry is struggling with weak demand, high costs, Chinese EV competition, and the painful transition away from combustion engines. Reuters recently reported that VW’s existing job-cutting plans may not be enough, with much bigger reductions under consideration.

The German automotive sector is not just another industry. It is one of the pillars of the German economy, employing hundreds of thousands of people directly and supporting many more through suppliers, logistics, engineering, finance, dealerships, and local services. Germany’s own car-industry lobby, the VDA, warns that the sector faces the potential loss of a further 125,000 jobs by 2035 if Germany and the EU fail to improve competitiveness.

Why this matters for Spain

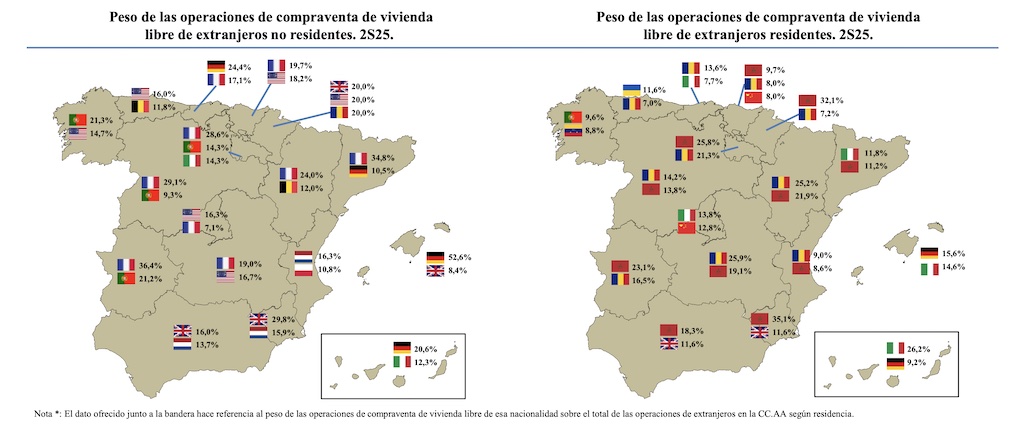

German buyers have long been one of the most important sources of foreign demand for Spanish property. According to notary figures (illustrated in the map above), they dominate the second-home market in the Balearics, where they account for more than half of foreign second-home purchases, and are also the leading group in the Canary Islands. They are number two in Catalonia and Cantabria.

For Spain as a whole, Germans have usually been the second-biggest foreign buyer group behind the British. They briefly took first place in 2021, but since the end of 2025 have slipped into third place behind the Dutch.

Registrar data already show German acquisitions of Spanish property declining year-on-year for three consecutive quarters. That does not yet amount to a slump: German demand remains well above pre-pandemic levels. But the direction of travel is no longer encouraging.

Could early retirement soften the blow?

There is one possible twist. A wave of restructuring in Germany might push some older workers into early retirement, and Spain could look attractive to those with decent pensions, savings, and a desire to make their money go further in the sun.

That may support some demand, especially from wealthier households. But it is unlikely to offset the broader damage if Germany’s industrial crisis deepens. Rising uncertainty tends to make people delay big discretionary purchases, and a second home abroad is about as discretionary as it gets.

The most exposed markets

The Balearics and the Canaries are the most exposed because German buyers play such an outsized role there. Mallorca in particular has spent decades building a market around German demand, from modest apartments to luxury villas. If German confidence and spending power take a serious hit, these markets will feel it first.

Catalonia could also be affected, though German demand there is less dominant and the region has other problems of its own, not least investor-hostile policies and high transaction costs.

The bottom line

A German car-industry crisis will not crash the Spanish property market on its own. Foreign demand is diversified, and British, Dutch, French, Belgian, Nordic, and domestic buyers all matter.

But if Germany’s industrial troubles turn into a wider economic malaise, Spanish second-home markets with heavy German exposure should expect weaker demand, longer selling times, and more price sensitivity. The Germans are not disappearing from Spain. But they may arrive with less confidence, tighter budgets, and a stronger instinct to wait and see.

Author: ![]() Mark Stücklin

Mark Stücklin

Posted on

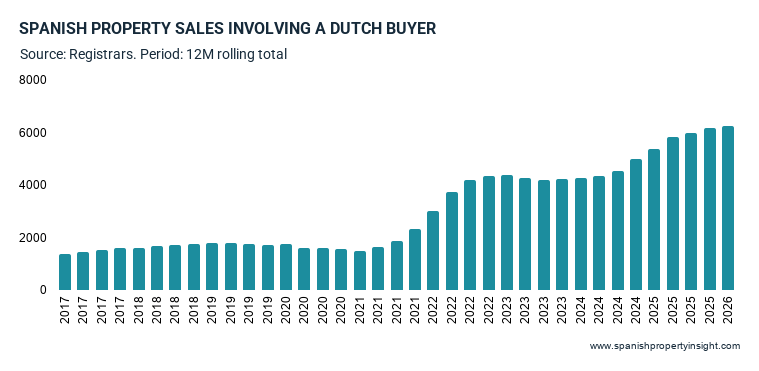

Dutch buyers continue to stand out in Spain’s foreign property market. The latest Land Registrar figures show demand from the Netherlands rising in Q1 2026, even as the wider foreign market declined.

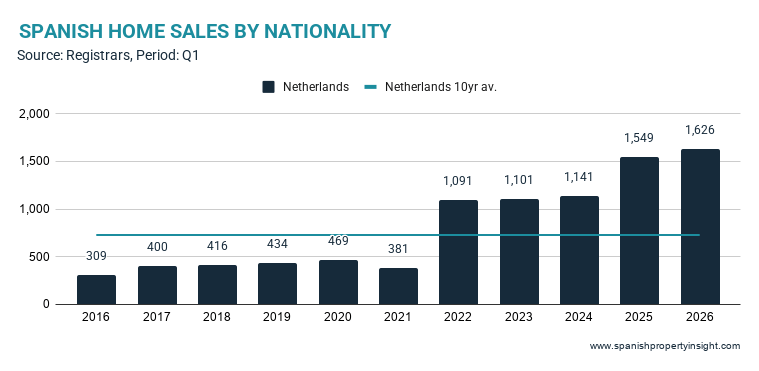

Spanish property acquisitions involving a buyer from the Netherlands reached 1,626 in the first quarter of 2026, according to the latest figures from the Spanish Land Registrars’ Association.

That was up 5pc compared with the same period last year, whilst total foreign demand fell by 3.2pc. So Dutch demand clearly outperformed the wider foreign market in the latest quarter.

More strikingly, Dutch demand was 123pc above its ten-year average for the first quarter, making the Netherlands one of the strongest-performing foreign buyer markets in Spain.

More than five times higher than in 2016

Taking 2016 as a base of 100, the Dutch buyer index stood at 527 in Q1 2026. In other words, Dutch demand is now more than five times higher than it was in 2016.

That compares with 193 for the foreign market as a whole, underlining how exceptional the growth in Dutch demand has been over the last decade.

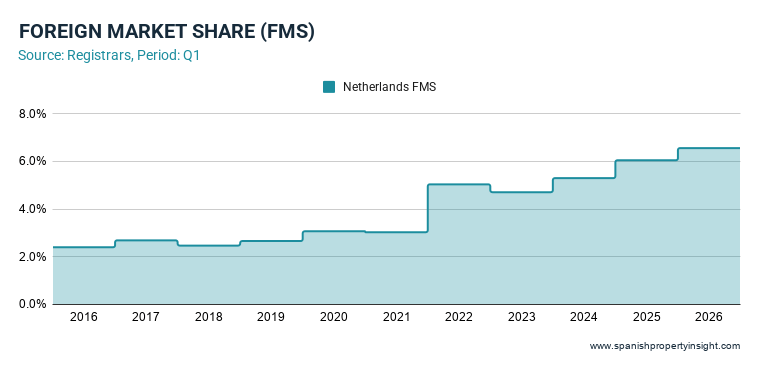

Market share hits a new high

Dutch buyers accounted for 6.6pc of all foreign purchases in Q1 2026, compared with a previous ten-year high of 6.1pc and a low of 2.4pc.

That means the Netherlands has moved from being a relatively small source market to one of the most important foreign buyer segments in Spain.

The rolling trend is still positive

Looking at the four-quarter rolling total, Dutch buyers acquired 6,232 homes in Spain over the latest twelve-month period.

That was up 1.2pc compared with the previous quarter, suggesting the underlying trend remains positive, even if growth is likely to be less spectacular than in the post-pandemic surge.

Demand drivers

What is driving this growth in Dutch demand? Along side the usual ‘pull factors’ like Spain’s sunshine, quality of life, and lower living costs, there are some recent ‘push factors’ like a recent wealth tax on savings and investments (seen as punishing cash savers), elevated transfer taxes and regulations on second homes/investment properties, and an overall expensive/tight domestic housing market. These make buying or holding additional property at home less attractive, encouraging capital flight and diversification into Spanish real estate as a lifestyle asset less burdened by Dutch fiscal pressures.

The takeaway is that Dutch demand remains one of the bright spots in Spain’s foreign buyer market. Whilst some traditional markets are cooling, Dutch buyers are still expanding their presence, supported by lifestyle demand, remote working, fiscal policy back home, and Spain’s relative value compared with property prices back home.

Sunset Symphony: Vera hosts weekly concerts beneath the summer sky

Tracy-Ann Oberman Refused Spain Flight

TUI’s new alcohol rule could change the traditional holiday warm-up

F1 Qualifying Results: 2026 Austrian Grand Prix times and grid positions

Terminal Patients In Poland Ask For The Right To Say Goodbye To Their Pets

Última Hora Del Terremoto En Venezuela, En Directo | Exteriores Eleva A 9 La Cifra De Españoles Fallecidos En El Doble Terremoto De Venezuela

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoF1 Qualifying Results: 2026 Austrian Grand Prix times and grid positions

-

%2 weeks ago

%2 weeks agoTerminal Patients In Poland Ask For The Right To Say Goodbye To Their Pets

-

America2 weeks ago

America2 weeks agoÚltima Hora Del Terremoto En Venezuela, En Directo | Exteriores Eleva A 9 La Cifra De Españoles Fallecidos En El Doble Terremoto De Venezuela

-

Latest2 weeks ago

EU Worries Jet Fuel Supply Situation To Worsen

-

airport liquids2 weeks ago

Malaga Airport to end liquids and electronics removal at security

-

America2 weeks ago

America2 weeks agoÚltima Hora Del Terremoto En Venezuela, En Directo | Venezuela Eleva A 920 La Cifra De Muertos Y Suma Más De 3.000 Heridos

-

car hire2 weeks ago

Spain tourists renting cars this summer warned over deposits, damage and hidden fees

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoWhen is the next F1 race? British Grand Prix schedule and details for 2026