Home sales

📣 Sales fall after last year’s surge

Heads-up! Q1 2026 housing numbers just published by the notaries – Spanish home sales fall back from last year’s high

The latest Q1 figures from the Spanish notaries suggest the market has finally come off the boil after a powerful run in 2025. Sales are down across all the main regions tracked here, though still comfortably above the ten-year average in most places.

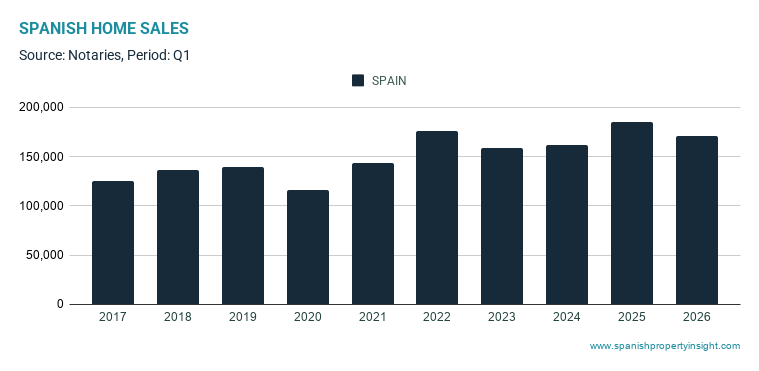

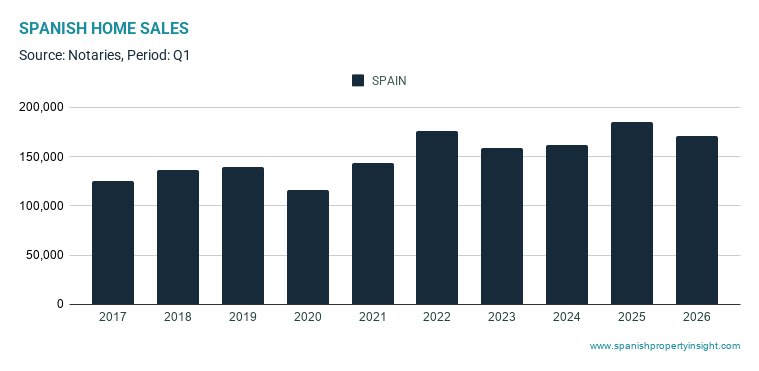

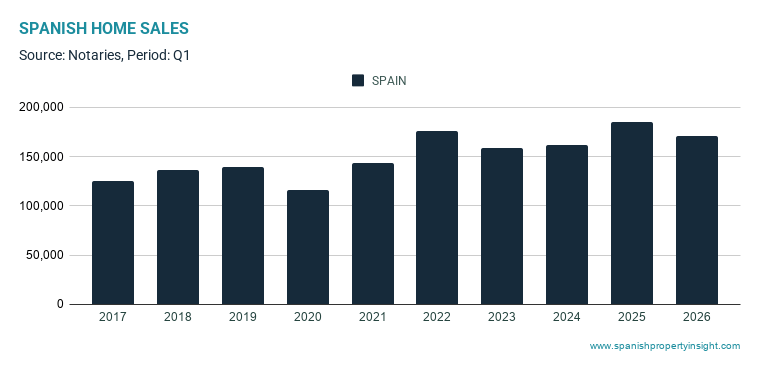

Spanish home sales reached 170,552 in Q1 2026, down 8% compared to the same quarter last year, according to the latest figures from the notaries. That sounds like a clear setback, and in annual terms it is. But context matters: Q1 2025 was the strongest first quarter in the series, so the comparison was always going to be demanding.

The national total is still 18% above the ten-year average, which suggests this is more of a cooling-off than a collapse, at least for now. In other words, the market has lost altitude, not fallen out of the sky.

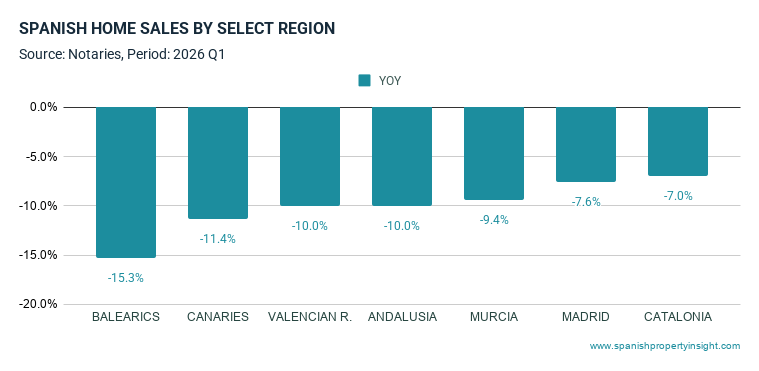

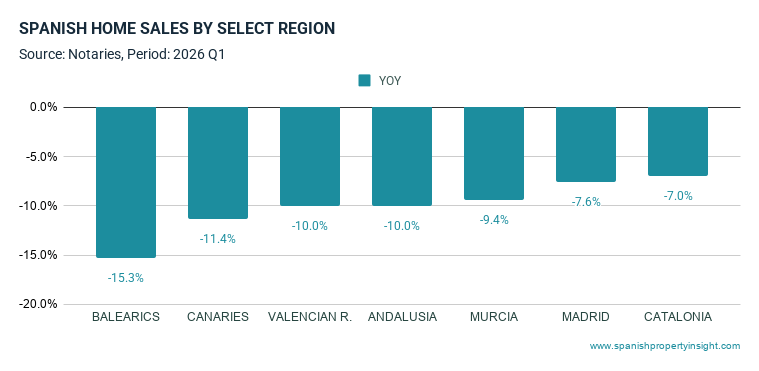

All the main regions covered by SPI’s data show annual declines. The sharpest fall was in the Balearics, where sales dropped 15%, followed by the Canaries down 11%, and Andalusia and the Valencian Region both down 10%. Murcia fell 9%, Madrid 8%, and Catalonia 7%.

That broad-based decline is the main message from the new data. This is not a local wobble in one overheated market, but a general easing in demand after a strong run.

Still above normal in most regions

The secondary point is that lower does not necessarily mean weak. Compared to the ten-year average, sales remain 31% higher in Murcia, 19% higher in Catalonia, 17% higher in Andalusia, 15% higher in the Valencian Region, and 3% higher in Madrid.

The exceptions are the islands, where sales were 13% below the ten-year average in the Balearics and 4% below in the Canaries. That may point to affordability limits biting harder in the most expensive and supply-constrained island markets, though we need more data before drawing firm conclusions.

The national market therefore looks like it has entered a softer phase after last year’s peak, but not yet a downturn of the sort that should have sellers reaching for the smelling salts. The next question is whether this is just a pause after a boom, or the start of a more sustained cooling cycle.

SPI’s full reports and data pages will dig into the regional detail, prices, mortgages, and foreign demand as more figures come in.

Prices keep rising despite lower sales

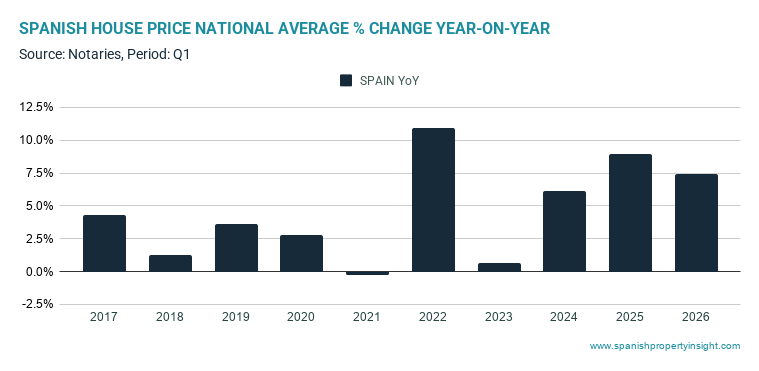

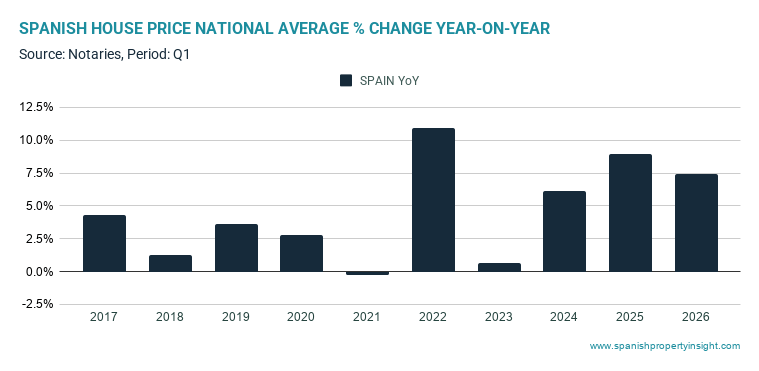

Prices tell a different story to sales. The national average price reached €2,022/sqm in Q1 2026, up 7% compared to Q1 2025, and the highest Q1 figure in the series provided.

That leaves national prices 34% above the ten-year average, underlining the point that falling sales have not yet translated into falling prices. This is not unusual at this stage of the cycle: transaction volumes tend to react first, whilst prices often lag behind. In some cycles, sales fall for several quarters but prices never turn negative.

So the Q1 picture is mixed but clear enough: demand has cooled after last year’s surge, but sellers are still holding the line on prices — for now.

Get the full picture

Don’t stop here. SPI’s in-depth reports go beyond the headlines with hard data and analysis of key markets and housing trends in Spain. Visit the reports section to get the full picture.

Heads-up! Q1 2026 housing numbers just published by the notaries – Spanish home sales fall back from last year’s high

The latest Q1 figures from the Spanish notaries suggest the market has finally come off the boil after a powerful run in 2025. Sales are down across all the main regions tracked here, though still comfortably above the ten-year average in most places.

Spanish home sales reached 170,552 in Q1 2026, down 8% compared to the same quarter last year, according to the latest figures from the notaries. That sounds like a clear setback, and in annual terms it is. But context matters: Q1 2025 was the strongest first quarter in the series, so the comparison was always going to be demanding.

The national total is still 18% above the ten-year average, which suggests this is more of a cooling-off than a collapse, at least for now. In other words, the market has lost altitude, not fallen out of the sky.

All the main regions covered by SPI’s data show annual declines. The sharpest fall was in the Balearics, where sales dropped 15%, followed by the Canaries down 11%, and Andalusia and the Valencian Region both down 10%. Murcia fell 9%, Madrid 8%, and Catalonia 7%.

That broad-based decline is the main message from the new data. This is not a local wobble in one overheated market, but a general easing in demand after a strong run.

Still above normal in most regions

The secondary point is that lower does not necessarily mean weak. Compared to the ten-year average, sales remain 31% higher in Murcia, 19% higher in Catalonia, 17% higher in Andalusia, 15% higher in the Valencian Region, and 3% higher in Madrid.

The exceptions are the islands, where sales were 13% below the ten-year average in the Balearics and 4% below in the Canaries. That may point to affordability limits biting harder in the most expensive and supply-constrained island markets, though we need more data before drawing firm conclusions.

The national market therefore looks like it has entered a softer phase after last year’s peak, but not yet a downturn of the sort that should have sellers reaching for the smelling salts. The next question is whether this is just a pause after a boom, or the start of a more sustained cooling cycle.

SPI’s full reports and data pages will dig into the regional detail, prices, mortgages, and foreign demand as more figures come in.

Prices keep rising despite lower sales

Prices tell a different story to sales. The national average price reached €2,022/sqm in Q1 2026, up 7% compared to Q1 2025, and the highest Q1 figure in the series provided.

That leaves national prices 34% above the ten-year average, underlining the point that falling sales have not yet translated into falling prices. This is not unusual at this stage of the cycle: transaction volumes tend to react first, whilst prices often lag behind. In some cycles, sales fall for several quarters but prices never turn negative.

So the Q1 picture is mixed but clear enough: demand has cooled after last year’s surge, but sellers are still holding the line on prices — for now.

Get the full picture

Don’t stop here. SPI’s in-depth reports go beyond the headlines with hard data and analysis of key markets and housing trends in Spain. Visit the reports section to get the full picture.

Spain’s housing market is starting to lose momentum as soaring prices, tighter mortgages, and worsening affordability begin to squeeze buyers out of the market, argues the think-tank Funcas.

After several years of boom conditions, the latest data suggests the Spanish property market may finally be entering a cooler, more selective phase—though a slump is not on the cards.

According to the latest figures from the Spanish National Statistics Institute (INE), home sales in Spain fell year-on-year for three consecutive months at the start of 2026. In the first quarter overall, transactions declined by 2.6%, with new home sales suffering an even sharper slowdown.

At the same time, house prices continue to rise strongly in many parts of the country, particularly in big cities and popular coastal markets. That combination—falling sales but rising prices—is often one of the first signs that a market is running out of steam.

Spain’s highly-regarded economics think tank Funcas says the market is now entering a phase of “stabilisation at a relatively high level” and warns that activity could contract further in coming quarters. The reasons are hardly mysterious: tighter financial conditions, a slowing economy, and households increasingly struggling to afford property.

In other words, prices kept rising long after buyers’ purchasing power stopped keeping up.

Buyers are being squeezed out

The affordability problem in Spain has become increasingly severe. Various studies from the Bank of Spain, the OECD and BBVA Research have warned for some time that buying a home now requires an enormous financial effort, especially for younger households and middle-income families.

Oxford Economics estimates that the average Spanish household now needs around eight years of gross income to buy a property—levels not seen since before the global financial crisis.

In regions like Catalonia the picture is even worse. Estimates suggest buyers need to save more than €500 per month for almost 13 years just to accumulate a deposit and buying costs.

At the same time, mortgage conditions are becoming more restrictive again after the recent rebound in Euribor rates and expectations of further European Central Bank rate hikes. Banks are also becoming more cautious as inflation and slower economic growth increase risks.

The result is obvious: fewer people can afford to buy at current prices.

Why prices are still rising

Despite the slowdown in demand, most analysts do not expect a dramatic collapse in prices. Spain still has a structural housing shortage, especially in major urban areas and popular coastal regions.

The Bank of Spain has repeatedly warned that the country is simply not building enough homes to meet demand. The IMF has also urged Spain to free up more land and speed up planning approvals to increase supply.

That shortage of housing is likely to prevent a 2008-style crash. But it could lead to a prolonged period of weaker sales activity, slower price growth, and price corrections in some overheated areas.

The Spanish property market increasingly looks like it is moving into a new phase: less buoyant, more cautious, and far more constrained by affordability than at any point in recent years.

For buyers, that could eventually mean more negotiating power. For sellers, it may mean the days of effortless sales at ever-higher prices are starting to fade.

Why Vejer De La Frontera Has Become The Food Capital Of Spain’s Cadiz

Cars & Coffee Sotogrande At Trocadero.

Quirky Almuñecar ship house receives fresh facade update in popular coastal spot

In The Final Stretch Of Colombia’s Presidential Campaign, Undecided Voters Are In High Demand

How To Get A Tourist Rental Licence In Andalusia (Spain) – Step-By-Step Guide 2025

Luis Rafael Sánchez: ‘Republicans Can’t Stand The Idea Of Puerto Rico Becoming A US State’

-

Abelardo de la Espriella2 weeks ago

In The Final Stretch Of Colombia’s Presidential Campaign, Undecided Voters Are In High Demand

-

New Developments3 weeks ago

New Developments3 weeks agoHow To Get A Tourist Rental Licence In Andalusia (Spain) – Step-By-Step Guide 2025

-

Bad Bunny2 weeks ago

Bad Bunny2 weeks agoLuis Rafael Sánchez: ‘Republicans Can’t Stand The Idea Of Puerto Rico Becoming A US State’

-

aemet3 weeks ago

Spain heatwave 2026: When the next extreme temperatures could hit and which areas may suffer most

-

Competiciones4 weeks ago

E

-

Costa Blanca North4 weeks ago

Benidorm unveils massive new SkyFest venue expecting 200,000 visitors this summer

-

buffet4 weeks ago

Toyo Japanese, Asian favours in Fuengirola

-

Costa Blanca South4 weeks ago

Torrevieja opens registration for Concilia Verano 2026 summer school